The statements, views and opinions expressed in this column are solely those of the author and do not necessarily represent those of this site. This site does not give financial, investment or medical advice.

The Duran’s Alex Christoforou and Editor-in-Chief Alexander Mercouris discuss the weakening Turkish lira which dropped more than 2 percent on Tuesday, after reaching 5.6125 against the US Dollar. Lira volatility comes after the United States halted delivery of equipment related to the F-35 fighter aircraft to Turkey.

Erdogan continues to push forward with the purchase of Russian S-400s, against US and NATO warnings to halt the order of the advanced Russian air defense system.

Remember to Please Subscribe to The Duran’s YouTube Channel.

Follow The Duran Audio Podcast on Soundcloud.

Turkish Lira Under Attack As U.S. Halts Shipment Of F – 35 Jet Equipment by The Duran

The Duran Quick Take: Episode 127. The Duran’s Alex Christoforou and Editor-in-Chief Alexander Mercouris discuss the weakening Turkish lira which dropped more than 2 percent on Tuesday, after reaching 5.6125 against the US Dollar. Lira volatility comes after the United States halted delivery of equipment related to the F-35 fighter aircraft to Turkey.

Via Reuters…

The disagreement over the F-35 is the latest of a series of diplomatic disputes between the United States and Turkey, foremost among which are Turkish demands that the United States extradite Islamic cleric Fethullah Gulen, differences over Middle East policy and the war in Syria, and sanctions on Iran.

U.S. officials have told their Turkish counterparts they will not receive further shipments of F-35 related equipment needed to prepare for the arrival of the stealth fighter aircraft, sources told Reuters on Monday.

Washington’s step to block delivery of the jet comes amid fears in the United States and other NATO allies, that radar on the Russian S-400 missile system will learn how to spot and track the F-35, making it less able to evade Russian weapons.

“The lira is under pressure as now the focus is back on structural problems for the Turkish economy,” said Nikolay Markov, a senior economist at Pictet Asset Management.

Is Turkey “City Zero” in Global Contagion, via Tom Luongo:

Last year Turkey’s lira crisis quickly morphed into a Euro-zone crisis as Italian bond yields blew higher and the euro quickly reversed off a major Q1 high near $1.25.

It nearly sparked a global emerging market meltdown and subsequent melt-up in the dollar.

This week President Erdogan of Turkey banned international short-selling of the Turkish lira in response to the Federal Reserve’s complete reversal of monetary policy from its last rate hike in December.

The markets responded to the Fed with a swift and deepening of the U.S. yield curve inversion. Dollar illiquidity is unfolding right in front of our eyes.

Turkish credit spreads, CDS rates and Turkey’s foreign exchange reserves all put under massive pressure. Unprecedented moves in were seen as the need for dollars has seized up the short end of the U.S. paper market.

Martin Armstrong talked about this yesterday:

The government [Turkey] simply trapped investors and refuses to allow transactions out of the Turkish lira. Turkey’s stand-off with investors has unnerved traders globally, pushing the world ever closer to a major FINANCIAL PANIC come this May 2019.

There is a major liquidity crisis brewing that could pop in May 2019.

Martin’s timing models all point to May as a major turning point. And the most obvious thing occurring in May is the European Parliamentary elections which should see Euroskeptics take between 30% and 35% of seats, depending on whether Britain stands for EU elections or not.

That depends on Parliament and the EU agreeing to a longer extension of Brexit in the next two weeks.

Parliament has created “Schroedinger’s Brexit,” neither alive nor dead but definitely bottled up in a box no one dares open. And they want to keep it that way for as long as possible. Their hope is outlasting Leavers into accepting staying in the gods-forsaken fiscal and political black hole that is the European Union.

But back to Turkey. To me this looks like a very dangerous game that Erdogan is playing with the markets to remind everyone just how fragile the financial system is. Now that a real Brexit back on the table thanks to the British Parliament his gambit takes on even more significance.

I don’t credit Erdogan with understanding this complexity anymore than I credit most Remainer MP’s understanding the true stakes of defying Brexit.

If he did he wouldn’t lift this foreign investor trap until Jean-Claude Juncker drank himself to death after a Hitlerian tirade of memetic proportions.

That’s the problem with politicians. Their own narrow interest has out-sized effects on the rest of the world because of the power they wield.

The core problem is that Turkey’s companies owe an enormous sum in corporate debt that is payable in dollars. What Erdogan has done is prioritize lira for them to pay their dollar obligations while barring anyone else from attacking the lira at the same time.

This morning at Money and Markets I talked why this is happening:

I don’t know for sure what’s happening here but I do know that the U.S. is playing hardball on anyone who is maintaining any economic ties to Iran, criticizing Israel and/or backing President Nicolas Maduro of Venezuela while we try and regime change him.

Turkey is doing all three of these things. And the combination of U.S. anger at Turkey’s sliding into the BRICS orbit, Turkey’s indebtedness and EU contagion risk creates a potentially explosive situation in credit and currency markets that Armstrong is now warning could become ground zero for the next financial crisis.

Erdogan’s proxy weapon in this fight is zombie banks in Europe. And not just any banks, some of the biggest banks in Europe. Zerohedge put out the list of the five European banks most exposed to Turkey according to Goldman Sachs.

With that disclaimer in mind, Goldman claims that Turkey exposure of EU banks is “limited in scope and scale” as Turkey accounted for <1% of total EAD and c.1% of Net Profit for Goldman’s EU banks coverage in 2018: of more 50 banks under Goldman coverage, five have Turkey exposure of >1% of total EAD, with gross exposure ranging from 10% of EAD for BBVA, 5% for Unicredit to 2% or less for ING (2%), BNP (2%) and ISP (1%). Also worth noting that European banks tend not to have 100% ownership of Turkish subsidiaries, so one needs to adjust for the actual shareholding.

The biggest banks in Italy, France and the Netherlands have multi-billion dollar exposure to a default on Turkish corporate debt.

| Bank | Total EAD (billions) | Turkey |

| BBVA | 699.8 | 68.2 |

| Unicredit | 837.9 | 41.1 |

| BNP Paribas | 1559 | 24.6 |

| ING | 890.3 | 15.3 |

| Intesa San Paolo | 616.5 | 3.9 |

Erdogan is staring at a major push-back from the U.S. and the EU over cozying up to Russia and it will not stop until he is removed from power.

As all of these interdependent systems, unintended consequences and perverse incentives have brought us to a very precarious moment in time.

Unspoken during all of the Brexit talk is the potential for real dislocation in the financial markets if the divorce is finalized to Brexiteer’s satisfaction. But the costs will be born hardest not on the working class but the financial and political class.

This is what is behind Project Fear and the slow motion betrayal of the Brexit Referendum of 2016. It is not the temporary inconvenience of having to pay 3% more for Italian wines or an extra ten minutes in line to take a holiday in France for the middle-class Briton Remainers who marched on London last weekend.

It is The Davos Crowd and their quislings in the British Civil Service and Brussels Byzantine Bureaucracy are the ones with trillions in assets at risk.

It is the British Deep State, so committed to the EU it helped back a coup against the President of the U.S. framing him as a Russian stooge straight out of a John LeCarre novel.

The mandarins who run the EU see their political project at risk. Turkey was a country slated to be subsumed by the murk of the EU.

And Erdogan put the kibosh on that after his country was nearly destroyed by U.S. incompetence in atomizing Syria. He has now emerged as a key political opponent of Brussels, as important as Viktor Orban in Hungary, Matteo Salvini and Luigi Di Maio in Italy or Vladimir Putin in Russia.

So it should come as no surprise that Turkey is emerging as the emerging market that comes under currency duress during this period of great uncertainty about the EU’s future.

Markets are finally taking these threats much more seriously now than they did last year. I told you then Turkey would survive. Qatar, China and Russia all came to Erdogan’s side to help Turkey through the shock.

But it was only a test of his resolve. It was a crucible to see if he could be brought back on side. And once Pastor Andrew Brunson was returned, the pressure on the lira mysteriously subsided.

But it’s clear with the way things have gone in Syria and with his opposition to Israel’s decisions recently that Erdogan is not redeemable as a NATO asset anymore. And the only reason Turkey hasn’t been kicked out of NATO is because treaties outlast leaders.

That’s why Brussels wants this Brexit deal and none other. It is a treaty which ensures the U.K. as a vassal state in perpetuity.

The U.S. equity markets just ended Q1 with the S&P 500’s highest closing quarterly price in history. The Dow Jones Industrials rallied to close just shy of 26,000. U.S. Treasuries are trading below the Fed’s benchmark rate throughout most of the yield curve.

And gold is holding onto $1300 despite furious selling above $1325 as traders scramble for dollars.

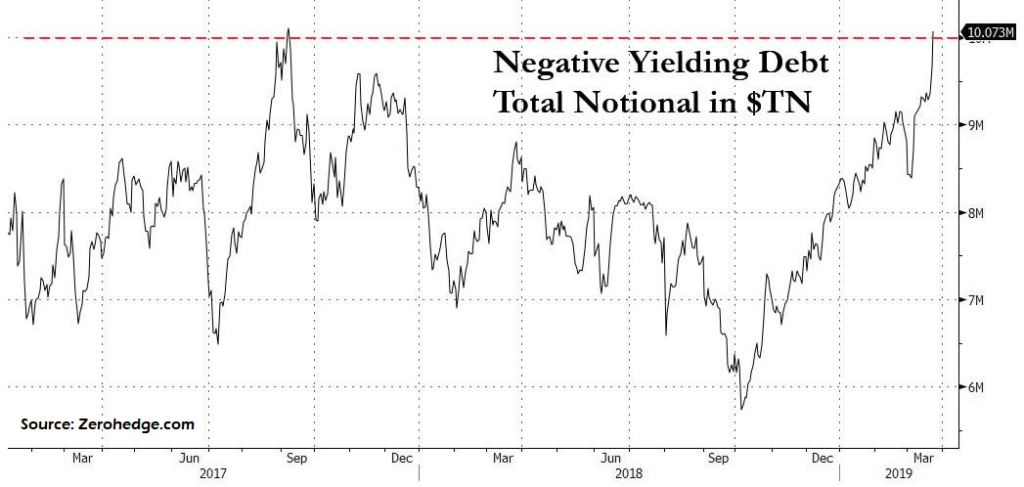

Since the equity markets peaked near the end of Q3 of last year, more than $5 trillion in debt globally has been pushed to negative yields as of Monday.

The number is not near a record $10 trillion.

The German yield curve is negative out to 10 years.

The sound you hear is the air leaving the room as the world wakes up to the fact that no one in charge has any clue as to how to fix any of the messes they have created.

The mad scramble for collateral has begun. And the zombie plague may have been unleashed in Istanbul.

To support more work like this and get access to exclusive commentary, stock picks and analysis tailored to your needs join my more than 235 Patrons on Patreon and see if I have what it takes to help you navigate a world going slowly mad.

The statements, views and opinions expressed in this column are solely those of the author and do not necessarily represent those of this site. This site does not give financial, investment or medical advice.

Erdogan is fed up with Nato, and rightly so. Let’s hope that Turkey will leave Nato soon.

This gives you reason never to import anything from the USA.

You will always remain at its mercy (if it has any).

Turkey (and other countries) should buy from Russia instead because Russia honours its agreements whereas the US time and time again does not. The US cannot be trusted..

Be kind. Americas lack of commitment to a deal is often a blessing in disguise. I took the US to Prove Russian tech by failing when Russia succeeded.

This is completely off topic, please forgive me, but i have been wondering about whatever happened to Mark Sleboda who was a regular on crosstalk. Does anyone know why he doesn’t appear anymore?

Let me see. Wait for parts for a flawed aircraft that’ll bankrupt a fickle economy or buy proven tech cheaper and re-allign the economy…? And we’re discussing Eddies buying habits…Why?

The US will not deliver the F35 to Turkey ? It’s a good job that will rejoice the Turks because that “lemon” is a poisonous one and many countries are experiencing reality and regret to have been bribed by Lockheed once again 🙂